The U.S. House of Representatives voted to pass the infrastructure bill that contained a provision that shook the crypto world. Financial regulators called on Congress to regulate stablecoins. In other words, crypto had a big week in Washington, D.C.

You’re reading State of Crypto, a CoinDesk newsletter looking at the intersection of cryptocurrency and government. Click here to sign up for future editions.

Taxes and stablecoins

The narrative

The U.S. House of Representatives voted in favor of the bipartisan infrastructure bill that contains two controversial crypto tax provisions, despite the ardent lobbying of crypto advocates who warned the provision would be terrible for crypto in the U.S. The bill passed the Senate without amendments back in August.

Why it matters

The Biden administration’s $1 trillion infrastructure bill contains a crypto reporting provision that appears to broaden the definition of a “broker” to potentially include crypto miners and developers, which would make compliance difficult, if not impossible. Another provision in the bill could make digital asset transactions – from purchasing cryptocurrencies to trading non-fungible tokens (NFT) – a felony if not reported correctly. Crypto proponents fear this could all be very problematic for the industry in the U.S., and could even push innovation offshore.

Breaking it down

Last Friday, the House of Representatives voted in favor of the bipartisan infrastructure bill. The bill now awaits President Joe Biden’s signature.

Despite some heavy lobbying by crypto lobbyists back in August to clarify the definition of “broker” as it applies to digital assets, the proposed bill passed the Senate without any amendments. The bill was introduced and voted through the Senate within a week in August.

While the bill was awaiting House approval, I spoke to some crypto tax lawyers in the U.S. about how things might play out if it is signed into law without amendments.

Nathan Giesselman, a partner at Skadden, Arps, Slate, Meagher & Flom LLP, told me that, as it is written in the bill, the provision runs the risk of capturing folks like miners and developers who don’t have the same customer information that a traditional broker might have, putting them in the awkward position of not being able to comply with the required reporting.

Now that the House has passed the bill, it’s clear that much will depend on how the U.S. Treasury Department interprets the definition of broker.

Back in August, reports surfaced indicating the Treasury Department might stick to the traditional definition of broker as laid out in the Internal Revenue Code, which would limit the term’s scope to only include dealers, barterers and other middlemen.

But David Zaslowsky, a partner at Baker & McKenzie and editor of the law firm’s blockchain blog, told me that it’s not clear if the Treasury Dept. will follow through.

“It is definitely the view of the Treasury [Dept.] that not everyone is reporting” who should be, Zaslowsky said.

Meanwhile, crypto lobbyists started pointing out that another potentially problematic provision in the bill had been totally overlooked.

The bill also proposed an amendment to tax code section 6050I to include digital assets. The original law put in place almost four decades ago requires anyone who receives more than $10,000 in cash in one transaction to report the sender’s personal information, including their Social Security number, to the government within 15 days.

Abraham Sutherland, adviser at crypto lobbying group Proof of Stake Alliance, wrote in a research report that this provision would apply broadly to all Americans who receive any kind of digital asset, from cryptocurrencies to NFTs.

“And under section 6050I, the failure to promptly and accurately verify and report the required information – information which might not exist – can be a felony resulting in prison time,” Sutherland wrote.

Jerry Brito, executive director of crypto lobbying group Coin Center, called the tax code amendment unconstitutional in a Twitter thread on Saturday. He also said there’s still time to “roll back” the provisions before they affect anyone as the provisions won’t take effect until at least 2024. According to Brito, options include working amendments into upcoming spending bills or introducing standalone bills.

“We’ve been working with several members of the House to introduce standalone bills to amend the new crypto tax reporting provisions. We would have over two years to get these passed,” Brito tweeted.

Meanwhile, the infrastructure bill has to be signed by the president, and the Treasury Dept. has to issue guidance on how these provisions will be enforced, particularly its interpretation of the term “broker.”

About that stablecoin report …

Last Monday, the President’s Working Group on Financial Markets finally released its long-awaited report on stablecoins. The report, put together by a group of financial regulators representing various U.S. government agencies, recommended that stablecoin issuers should be subject to the same federal oversight as banks. The report also suggested that should Congress fail to take regulatory action, financial regulators will step in and establish oversight through the interagency Financial Stability Oversight Council.

I spoke to some of the top stablecoin issuers as well as crypto lobbyists to see what they thought about the report and noticed a discrepancy in their reactions. Some stablecoin issuers like Circle and Tether welcomed the prospect of being treated as regulated banks. But crypto lobbyists were not as enthusiastic about some of the report’s other implications.

Coin Center and the Chamber of Digital Commerce (CDC) said the oversight suggested in the report could put a damper on innovation and subject stablecoins to stricter rules compared to other payment systems like PayPal that offer similar services. Lobbyists also fear that things could get messy if multiple government agencies try to regulate the space.

Cornell economist Eswar Prasad told me the crypto industry wants the best of both worlds and is trying “to walk a fine line between benefiting from the legitimacy provided by government oversight while trying to stay clear of extensive and intrusive regulation that deters innovation.”

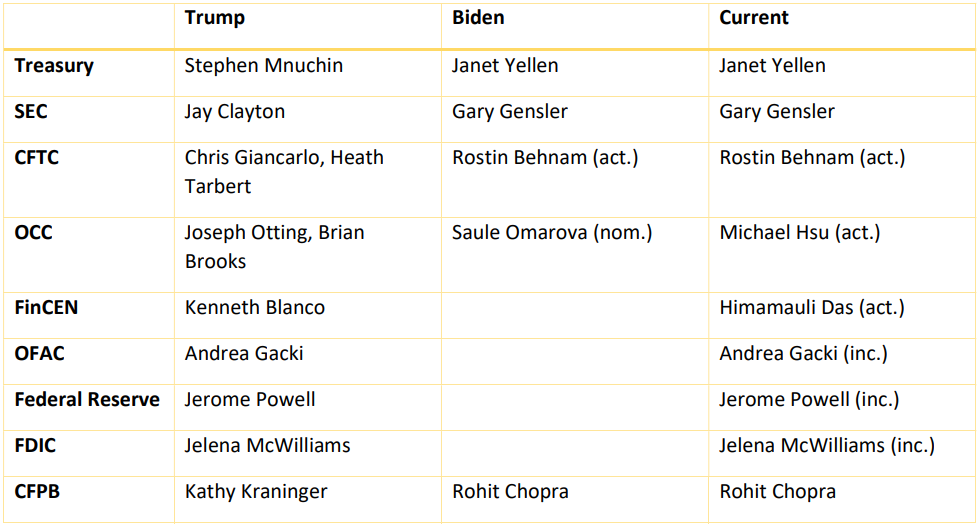

While appearing on Monday’s episode of CoinDesk TV’s “First Mover,” Acting Comptroller of the Currency Michael Hsu said that the term “innovation” is getting thrown around a lot. There are some areas where we want unfettered innovation, Hsu said, but stablecoins may not be one of those areas.

“You want your money to be stable. You want it to be reliable. You want it to be there in good times and bad times and not have to think about it. If you innovate too much in that space, you’re going to get a wide range of outcomes that some of which are not going to be good,” Hsu said.

Biden’s rule

Last week, President Biden said that he will announce his choice for the chair of the Federal Reserve “fairly quickly” but did not specify whether it’s going to be Jerome Powell, whose term as chairman will expire in February.

Elsewhere

- In Craig Wright Trial, Plaintiffs Lay Out Pattern of Fraud, Deceit and Hubris: The civil trial Ira Kleiman v. Craig Wright, involving the self-proclaimed inventor of bitcoin, Craig Wright, kicked off last week in Miami. Kleiman is suing Wright for what he claims to be his brother Dave’s share of a sum of bitcoin currently valued at $66 billion.

- Europe’s MiCA Crypto Rules Are Coming Soon. Here’s Why They Matter: The European Union will soon ratify a 168-page proposed framework for regulating crypto assets, which could set up a passportable license so crypto firms can expand through the bloc easily. But, drafted with Facebook’s Diem stablecoin project in mind, a great portion of the framework lays out rules for stablecoin issuers with some additional rules for larger issuers.

Outside CoinDesk

- (Vice) Apparently, hackers are forcing Instagram users to publish hostage-style videos asking followers to participate in get-rich-quick schemes in exchange for their accounts.

- (Reuters) An increasing number of female artists, coders, entrepreneurs and investors are not only embracing cryptocurrency and NFTs, but are advocating for other women to join and carve out a space for themselves in the blockchain movement.

If we don't see $70,000 #Bitcoin this week, I will fast for 7 days.

— Mike Alfred (@mikealfred) November 8, 2021

Leave a Reply